Car insurance in Florida is expensive — often significantly higher than the national average.

If you're trying to figure out how to save money on car insurance in Florida, you're not alone. Between rising premiums, confusing coverage requirements, and constant rate changes, many insured drivers end up overpaying without realizing it.

In this guide, we’ll break down why Florida car insurance costs so much and, more importantly, how you can lower your premium with practical, proven strategies.

Why Have Car Insurance in Florida?

In Florida, car insurance is not optional; it is a legal requirement for anyone who wants to register or drive a vehicle with four or more wheels. To stay compliant with Florida car insurance laws, drivers must maintain a minimum of $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL).

PIP helps cover your own medical costs after a crash, regardless of fault, while PDL pays for damage you cause to someone else’s property. Florida also requires continuous coverage for as long as the vehicle is registered, even if the car is not being driven.

Illegally driving uninsured or allowing your coverage to lapse carries heavy penalties. Florida can suspend your driver’s license, registration, and plates for a lapse in coverage, and getting them back often requires a reinstatement fee between $150 and $500.

How Much Car Insurance Should I Purchase in Florida?

For readers wondering how much car insurance they should have, the Florida minimum auto insurance requirement is only a starting point. The legal minimum of $10,000 in PIP and $10,000 in PDL may satisfy the state, but it does not always safeguard from the real cost of a serious accident.

Repair bills and out-of-pocket expenses compel many Floridians to carry more than the minimum car insurance coverage, even when they are mainly focused on saving money. Depending on driver specifics, opting for above-minimum coverage is often the most financially beneficial. It avoids turning one wreck into a long-term setback.

Can You Get Car Insurance Without a License in Florida?

Many Florida residents, such as parents of licensed drivers, wonder if they can acquire vehicle insurance without holding a license themselves. In practice, yes, but the process is usually more restrictive.

In such cases, many Florida insurers require you to name the licensed primary driver on the auto policy, and some may list you as an excluded driver if you are not licensed. That distinction is important: owning a policy is not the same as being legally allowed to drive.

Understanding The Price of Car Insurance in Florida

The first step towards saving money on Florida car insurance is understanding how much the premiums typically cost. The short answer is: more than almost anywhere else in the country. Florida consistently ranks as one of the most expensive states for insured drivers, with car insurance premiums costing between 44% and 68% more than the national average.

Florida Car Insurance Average Cost: 2025-2026 Data

To understand how much car insurance costs in Florida, you have to look at the level of protection people typically choose. As of early 2026, the price gap between minimum coverage and full coverage is wider than ever.

- Full Coverage: The average cost of Florida car insurance for a full coverage policy (including liability, collision, and comprehensive) is approximately $3,884 per year (about $324 per month.)

- Minimum Coverage: For those seeking only the state-mandated $10,000 PIP and $10,000 PDL, the average cost is roughly $1,056 to $1,722 per year ($88 to $144 per month.)

- Statewide Average: Across all policy types, the average car insurance premium for Florida sits at approximately $2,289 per year ($191 per month.)

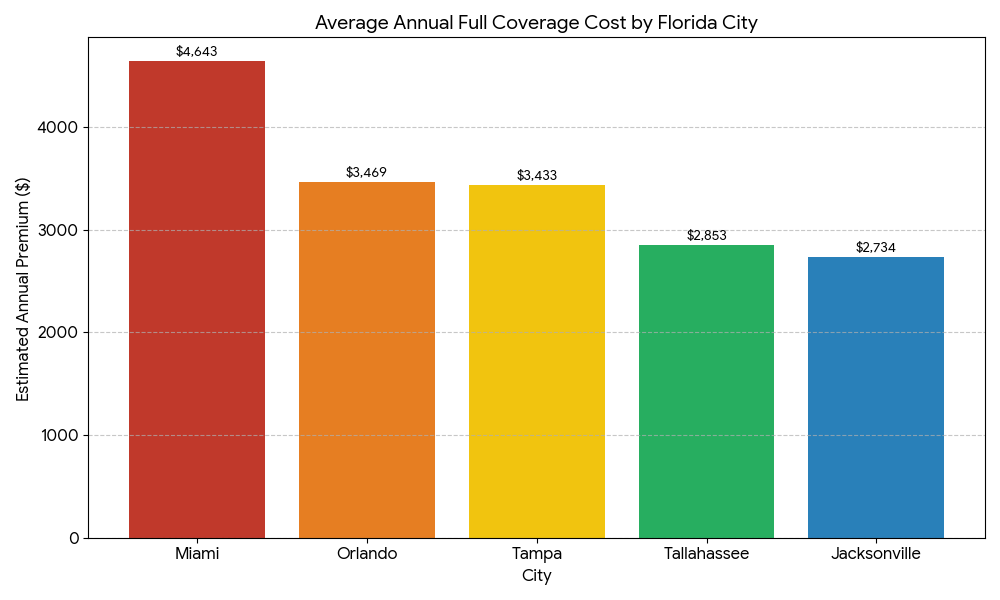

Florida Car Insurance Price by City

Where you park your car in Florida is one of the biggest factors in your car insurance rate. High-density areas with more traffic and higher fraud rates, like Miami, see the steepest prices.

If you live in a high-cost city like Miami or Orlando, your base rate starts higher, but that doesn't mean you have to accept a high bill. In Florida, high-density cities often have more insurance carriers competing for your business. By using an agent to compare these localized rates, you can often find discounts that online algorithms miss.

Why is Florida Car Insurance So Expensive?

Understanding why car insurance in Florida is typically a higher price than other states involves looking at a combination of unique legal structures, environmental risks, and social factors. Here is the breakdown of the systems in place driving those high premiums.

Florida’s No-Fault System

Florida is one of only twelve states that operates under a no-fault car insurance system. This is a system in which your own insurance company pays for your medical treatments and certain economic losses (like lost wages) after an accident, regardless of who caused the crash.

A correlation of this no-fault system is Personal Injury Protection (PIP) coverage. Your PIP will typically pay 80% of necessary medical expenses and 60% of lost wages, capped at Florida's $10,000 limit.

While intended to reduce small-claims litigation and speed up payments, the "guaranteed" nature of PIP payments has historically made Florida a target for inflated medical billing and staged-accident fraud, which drives up premiums for everyone.

Primary Factors Driving Up Florida's Car Insurance Rates

Beyond the the state’s no-fault system, there are several other factors influencing how car insurance is calculated by Florida providers:

- High Population Density and Traffic: Florida is the third most populous state. Urban centers like Miami, Tampa, and Orlando have extremely high traffic congestion, which statistically leads to a higher frequency of accidents and claims.

- Uninsured / Underinsured Driver Issues: Despite state law requiring vehicles on the road to be insured, Florida has one of the highest rates of uninsured drivers in the country, with estimates ranging from 15% to 20% of all motorists. This forces insured drivers to pay more for Uninsured Motorist (UM) coverage to protect themselves.

- Weather and Storm Risk: Florida is uniquely vulnerable to hurricanes, tropical storms, and flooding. Because comprehensive coverage pays for storm-related damage (like a tree falling on a car or flood damage), insurers charge higher rates to offset the massive payouts seen after major weather events.

- Litigation and Fraud Environment: Florida has historically faced a high volume of insurance lawsuits. Until very recent reforms (such as the 2022/2023 legislative sessions), "one-way attorney fees" and "assignment of benefits" (AOB) abuse allowed for excessive litigation costs that were passed on to consumers.

- ZIP-Code Risk Differences: Insurance companies calculate risk down to the neighborhood level. Factors like local crime rates, vehicle theft statistics, and even the number of litigated claims in your specific ZIP code can cause your rate to differ significantly from someone just a few miles away.

- Repair and Medical Cost Inflation: As vehicles become more advanced (with sensors and cameras), they become more expensive to repair. Coupled with the rising cost of medical care in Florida, insurers must raise premiums to keep up with the increasing size of claims.

7 Ways to Save Money on Florida Car Insurance

Knowing how to save money on car insurance is essential in a high-premium market like Florida. While rates are influenced by statewide trends, your individual choices as a driver play a massive role in your final quote. Here are seven actionable ways to cut costs on Florida auto insurance without sacrificing the coverage you need.

1. Avoid Using Your Car

If you live in a walkable area of Florida or use alternative commuting methods, you could save significantly on your monthly car insurance rate.

Additionally, many Florida insurers offer "pay-per-mile" programs or telematics-based discounts. This involves using a plug-in device or mobile app to track your mileage and safe driving habits. The longer you use these methods, the more you can prove to your carrier that you are a lower risk than the average commuter.

2. Regularly Compare Florida Auto Insurance Quotes

In Florida, the market for car insurance quotes is incredibly volatile and varies by location, with carrier rates changing monthly based on new data for specific ZIP codes. If you haven't shopped for a new rate in the last six to twelve months, you are likely overpaying. To get the most savings on car insurance in Florida, frequently price shop to ensure you're still getting the best deals.

3. Improve Your Credit-Based Insurance Score

In Florida, auto insurers use a credit-based insurance score (CBIS) to help determine your premium. While not exactly the same as your regular credit score, your CBIS still reflects your payment history and total debt, allowing companies to gauge the long-term risk of you filing a claim. Statistically, drivers with poor credit see rates that are nearly double those of drivers with excellent credit.

You can improve your CBIS by focusing on these key factors:

- Prioritize Payment History (40% of score): This is the most weighted factor. Ensure you pay every bill on time; if you’re behind, catch up as soon as possible to stabilize your history.

- Manage Outstanding Debt (30% of score): Keep your credit card balances as low as possible. High "utilization"—using too much of your available limit—is a red flag for insurers.

- Protect Your Credit Age (15% of score): Avoid closing old accounts, as a longer credit history demonstrates more stability to a Florida insurer.

If you want a personalized plan to optimize your credit and unlock lower insurance rates, the Yesis Gomez insurance team offers a direct referral to a top-rated, Miami-based credit specialist.

4. Maintain Accurate Vehicle Information

Accurately listed vehicle specs are your best friend when it comes to saving on Florida auto insurance premiums. Whenever you get an oil change or service, a summary of your vehicle information is updated and easily searchable in national databases.

If your insurance policy lists 15,000 miles a year but you actually only drive 5,000, you are paying for risk that doesn't exist. On the opposite end, if you drive more than your amount stated to insurers, they may find out and increase your premium.

To check if your insurer is using the correct data to calculate your rate, you can use the Florida Department of Highway Safety and Motor Vehicles (FLHSMV) Check Tool to perform a VIN check on your Florida registered vehicle. This portal allows you to see exactly what is on record regarding your vehicle's title and history, helping you ensure that the stats your insurance company is using—such as your vehicle’s safety equipment and registration details—are 100% accurate.

5. Bundle Your Insurance Policies

One of the most effective ways to save money on Florida car insurance is through bundling. By placing your auto, homeowners, or renters insurance with the same agent or carrier, you can often cut costs by 10%-25% across all policies.

Yesis Gomez can assist you in bundling your auto insurance to ensure you are capturing the maximum multi-policy discount available in the Florida market.

6. Ask About Specific Discounts

Don't assume your Florida car insurance company has applied every discount you're eligible for. Always ask about:

- Good Driver Discounts: For those with a clean record for 3+ years.

- Defensive Driving: Involves completing an approved safety course.

- Student Discounts: "Good Student" rewards for high GPAs.

- Safety Features: Discounts for vehicles with daytime running lights, VIN etching, or GPS tracking.

- Mature Driver Discount: For Florida drivers over the age of 55 who have completed an approved safety course.

7. Consult a Florida Car Insurance Agent

Many motorists think that hiring a Florida car insurance agent is a luxury that adds to their bill, but the truth is that professional guidance usually ends up paying for itself. Because agents have direct access to exclusive carrier markets, they can pinpoint specific discounts or redundant coverages that automated websites typically miss.

The flip side is that navigating these savings independently is often a second full-time job. Comparing quotes, deciphering policy jargon, and verifying state compliance takes hours of research—all while your current bills continue to roll in. A Florida auto insurance agent handles that legwork for you. They can restructure your policy to cut costs before your next monthly payment is even due.

Is a Florida Car Insurance Agent Right for Me?

Deciding whether to use an agent usually depends on how complex your daily life is. If you only drive a few miles a week or own a single vehicle, a basic insurance platform might be enough. This approach works for drivers are only seeking the absolute minimum Florida coverage to keep their vehicle legal and drivable.

However, an agent is essential once your lifestyle involves multiple drivers, a daily commute, or using your vehicle for deliveries or rideshare. Additionally, if you have assets like a home or savings to protect, it becomes beneficial for a professional agent to coordinate your coverage with your asset risks.

Ready to Lower Your Florida Auto Insurance Bill?

When you want a long-term strategy to save money on Florida car insurance premiums, Yesis Gomez and her team provide the specialized oversight required to secure your financial future. Instead of settling for a generic policy, you get an advocate who understands how to navigate the specific risks and rising costs of the Florida market.

Contact Yesis Gomez today for a comprehensive review of your Florida auto insurance plan.